By Daniel Lancaster, CFA® | The Wealth Expedition

This content is for informational and educational purposes only and should not be considered individualized investment advice.

When it comes to building long-term wealth, investors have a number of ways to invest. A key question that investors eventually face is: should you use a mutual fund or an exchange-traded fund (ETF)?

The right vehicle can make a meaningful difference in costs, tax-efficiency, flexibility, and ultimately investment performance.

And in the world of compounding returns, that can mean a life-changing difference.

In this article we’ll cover the fundamentals of both investment vehicles, compare fees, tax implications, trading mechanics, and whether one or both fit within your strategy—especially when you’re targeting growth over decades.

Within The Wealth Expedition, investing isn’t just about retirement. It’s also about creating flexibility and opportunity today.

Saving for retirement is one milestone, but building an opportunity fund—a pool of capital you can use for lifestyle upgrades or business ventures—can accelerate your journey toward financial freedom.

Here we’ll examine ETFs vs. mutual funds within the context of long-term retirement investing and intermediate- and short-term investing for opportunity.

What is a Mutual Fund?

How Mutual Funds Work

Think of a mutual fund like a well-oiled machine, made up of individual parts.

Those parts might be stocks, bonds, alternatives or cash.

Rather than trying to do it all yourself, you’re buying a pre-packaged and pre-constructed basket of securities. That means if you agree with the goal and the strategy to achieve it, then you can leave the deeper research, trading and strategic positioning to professionals.

In short, a mutual fund is a pooled investment vehicle that combines money from many investors and invests it into a portfolio of stocks, bonds, or other assets.

Key Features and Costs

Pricing: When you buy or sell shares of a mutual fund, your transaction is executed at the fund’s net asset value (NAV), typically calculated at the end of each trading day. This means any buy or sell order for fund shares executes only at the end of a trading day.

Minimums: Some mutual funds may require a minimum investment amount.

- Transparency: Many publish their top 10 holdings monthly, but rarely the full portfolio. Some disclose the full portfolio quarterly. More active funds guard their secrets to prevent copying.

- Structure: Most mutual funds charge an expense ratio: an annual percentage of the fund’s value, typically ranging between 0.1%-1.5%. According to ICI Research, the average, as of 2023, stood at 0.42%. Some additionally charge fees called loads (either when you buy or when you sell) or 12b-1 fees (which are part of the expense ratio).

Management style: Many mutual funds are actively managed, meaning they stray meaningfully from their benchmark, the stock market index they’ve chosen as their measuring stick. More action within the portfolio means higher fees, with the aim to achieve their stated goal. There are also index mutual funds, which are highly passive and attempt to match the market, requiring lower cost.

- Fractional shares: Mutual funds allow investors to buy fractional shares, meaning that if you have $1,000 to invest, and each share is priced at $57, then you can purchase 17.54 shares. You don’t need to have exactly the amount to buy a full share.

Liquidity: While you can redeem mutual fund shares daily, you cannot trade them intraday like a stock. Your price is set at market close.

Mutual funds remain a core option for many investors, and often constitute the main choice of investments within tax-advantaged accounts like 401(k)s and 529 plans. They’re also well-suited for those seeking professional management, ESG investing, automatic investment plans, or specialized strategies.

What is an ETF?

How ETFs Work

An exchange-traded fund (ETF) is very similar, but with important differences.

Think of this as the compact, sleek model that’s more convenient to pack along with you on a journey.

It doesn’t mean it’s better per se. It just means it’s simpler.

And it’s particularly useful for certain types of investors over others. But more on that to come.

An ETF is also a pooled investment vehicle, with some key differences from mutual funds.

Key Features and Costs

- Pricing: ETF’s prices fluctuate in real time as investors buy and sell shares on the market. Although an ETF’s market price typically stays close to its net asset value (NAV), small differences can occur due to supply and demand.

- Minimums: ETFs generally have no minimum investment beyond the price of a single share, though many brokers now allow you to buy fractional shares.

- Transparency: Most ETFs publish their full list of holdings every trading day for the public.

- Structure: Many ETFs, especially passive ones, have very low expense ratios and typically no loads or 12b-1 fees.

Tax efficiency: One of the major advantages of ETFs over many mutual funds is that when an investor buys or sells shares, the managers don’t have to buy/sell securities that make up the ETF (leading to fewer taxable events than mutual funds).

- Management style: Most ETFs are passively managed, meaning they choose a largely rules-based benchmark to follow and stick to it. This requires less ongoing human decision on the manager’s part, as well as less trading, resulting in lower fees on average.

- Fractional shares: Historically, ETFs could only be purchased in whole shares. Recently, however, some firms have introduced the ability to purchase fractional shares similar to mutual funds (depending on broker).

Liquidity: ETFs can be bought or sold intraday like stocks, meaning they don’t have to wait until end-of-day to trade like mutual funds.

For long-term growth, investors who prefer low cost, tax-efficient, diversified exposure, ETFs are increasingly the preferred vehicle.

ETF vs Mutual Fund Strategy (Passive vs Active)

When comparing ETF vs mutual fund performance, one major axis hinges on the passive vs active strategy.

ETFs tend toward more passive strategies. Mutual funds can be either, but typically stand out for their active strategy capabilities.

Passive ETFs

Track an index (e.g., S&P 500, Total Stock Market) with minimal turnover and low fees.

Because of their low cost, they reduce the “drag” on returns and compound more effectively over time. Many studies suggest that active strategies struggle to outperform after fees and taxes.

Ideal for long-term growth: you buy, hold, diversify globally, let compounding and time work.

Active Mutual Funds

The manager attempts to beat a benchmark, which involves higher expense ratios, greater turnover, and more style risk.

They may underperform after fees and taxes; therefore, when used for long-term growth, the odds are stacked against them. Some investors choose them for intermediate-term goals or specific tactical allocations (e.g., small-cap, emerging markets, thematic).

A blend can work: passive core (ETFs) + tactical active sleeve (mutual funds) for diversification of strategy and correlation.

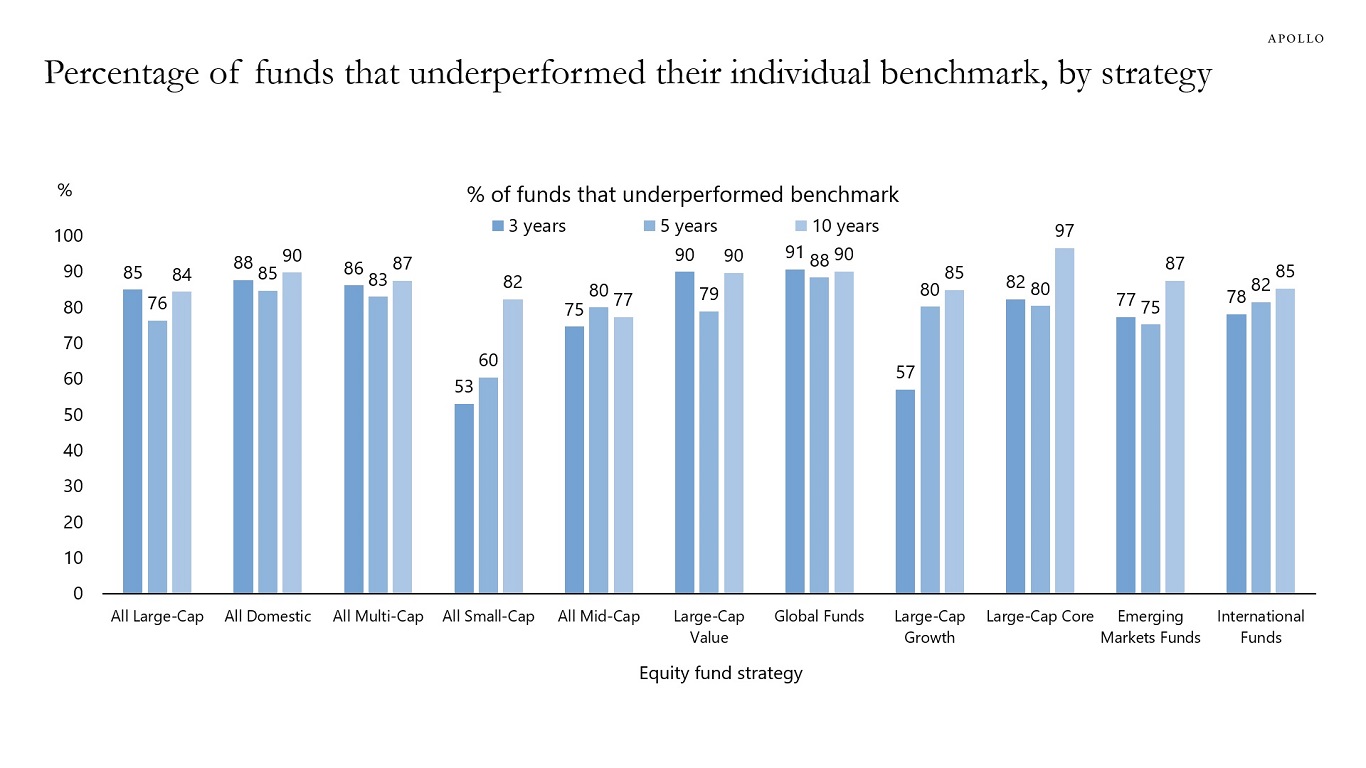

Studies clearly show that passive management, on average, tends to beat active management. According to Apollo Academy’s 3-, 5- and 10-year study, the active portfolios that outperformed generally ranged between 10%-15% of available funds. That means, if you threw a dart at a list of mutual funds, you had about an 85%-90% chance of landing on one which would produce lower returns than its passive counterpart.

Correlation & diversification nuance

But don’t write off active portfolios just yet.

The key to successful investing is weighting odds in your favor over a particular timeline. And risk management is a huge part of that.

What is the core way we can manage risk? One word: diversification.

Diversification isn’t about just owning lots of things. It’s about owning things that behave differently.

Correlation measures that relationship on a scale ranging from +1 (perfectly aligned) to –1 (moving opposite each other).

Blending passive ETFs with active mutual funds (or even hedge funds) can reduce overall volatility by mixing strategies that respond differently to markets. Over a 20-30+ year horizon, this has the potential to improve your risk-adjusted growth.

In many portfolios the optimal path is:

Core allocation: low-cost passive ETFs

Satellite allocation: active mutual funds that seek to outperform a certain benchmark or achieve a goal that a passive index cannot.

Rebalance periodically to maintain target asset allocation, adjusting the target for major life changes.

ETF vs Mutual Fund Fees

One of the clearest differences between ETFs and mutual funds is cost. When considering the long-term comparison of ETF vs mutual fund performance, cost is a major driver of long-term outcomes.

While it’s true that cost isn’t everything, it does play a role. If you’re paying 1% as an expense ratio but averaging 2% annual outperformance, then the cost is worth the value.

But that’s rarely how it turns out in practice, even among hedge funds.

First, let’s examine the facts:

Expense ratios: Passive ETFs can exhibit expense ratios as low as 0.03% (in very competitive niches) vs higher ratios of 2%+ for actively managed mutual funds.

Loads, 12b-1 fees, redemption fees: These upfront fees at purchase, or back-end fees when sold, are common in many mutual funds; ETFs avoid these. There are some no-load mutual funds which avoid these.

Trading costs & bid/ask spreads: For ETFs, you may pay brokerage commissions (though many brokers now offer $0 trades) and should consider the bid/ask spread (what you can sell it for vs what you can buy it for at any given moment, which is not the exact same price); mutual funds may have no commissions but can incur the other costs mentioned in the previous point.

Impact on growth: Lower fees mean more net capital remains invested and compounding runs more efficiently over decades.

Therefore, when considering which is better in the ETF vs mutual fund discussion, fees strongly favor ETFs—especially when you’re using passive strategies, which regularly outperform most active managers after fees. This is especially important for long-term compounding growth.

ETF vs Mutual Fund Tax

Tax efficiency is a second major dimension to compare.

Many long-term investors hold at least some funds in taxable accounts (non-retirement accounts).

This is particularly relevant within The Wealth Expedition for those who are building their opportunity fund. This opportunity fund is intended for either 1) use as a discretionary fund for lifestyle upgrades or 2) bridging to entrepreneurship for far higher potential ROI.

The difference between ETF vs mutual fund tax treatment becomes meaningful for those who are saving outside of tax-advantaged accounts.

When an investor (like yourself) sells shares of a mutual fund, the fund may need to sell underlying securities, thereby generating capital gains distributions to all shareholders—even those who did not sell.

ETFs use an in-kind creation/redemption mechanism, meaning securities can be swapped rather than sold, reducing capital gains distributions and enhancing tax efficiency.

Studies indicate ETF investors may incur lower “tax drag” compared to mutual fund investors over time. This subtle advantage compounds.

That said, within tax-advantaged accounts (401(k), IRA) the tax efficiency difference is irrelevant, so the choice here depends more on cost, strategy, and vehicle flexibility.

So if you’re investing in a taxable account, the question of whether ETFs are better than mutual funds often leans heavily toward ETFs because of tax structure and compounding effects.

Individual Stocks vs ETFs vs Mutual Funds

So why pay anyone an expense fee at all?

Why not simply be your own portfolio manager from the ground up? After all, it’s not that difficult to pick 30-50 stocks you think will do well. That way you avoid the management fees altogether!

For a rare few, this might be the right path. But not so for most investors.

That’s because stocks, by themselves, feature a significant degree of what is called “unsystematic risk.” That means there is a large degree of risk holding any particular company which does not add likelihood to long-term returns.

The purpose of diversification is to reduce this unsystematic risk as much as reasonably possible, while maintaining the good kind of risk (systematic risk) which is the reason markets reward investors over the long-run.

Good diversification reduces unnecessary risk without meaningfully reducing expected long-term return.

But good diversification is more than simply picking one’s favorite stocks. It’s far more involved, spanning research across countries, sectors, stock styles, market cap, and asset classes, with a strong focus on correlation among assets.

Some investors have the time, knowledge and energy to do this on their own—but most don’t.

That’s why paying a reasonable expense fee can be a far better use of one’s time to get the benefit of professional management without the time-intensive work of micro-managing one’s own portfolio.

In simple form: If your goal is to build wealth steadily over years/decades, holding low-cost broad-market ETFs is often superior to picking individual stocks (unless you’re exceptionally skilled) or paying high fees in actively managed mutual funds.

ETF vs Mutual Fund: Which Is Better?

So with all the above in mind, here’s how to determine which is better, ETFs or mutual funds, for your portfolio.

For most investors, when uncertainty creeps in, defaulting to passive is generally the wiser move. None of us are perfect forecasters, and in the world of investing, conviction matters. If, on a scale from 1 to 10, your confidence in an active strategy sits at a 7 or even an 8, that’s not enough. In investing, being merely “warm” toward an active idea usually isn’t worth the risk, especially when long-term evidence suggests that passive strategies outperform the majority of active funds after fees and taxes.

Still, there are exceptions — and recognizing them takes discernment. Expenses and manager ownership can serve as helpful screening tools.

Ask yourself: Does this manager charge justifiable fees for their skill and access, or are the costs eating into my compounding potential?

And does the manager have meaningful “skin in the game” through personal investment in their own fund?

If the answers don’t inspire confidence, it’s often best to stay away.

For those who want to balance both worlds, a core–satellite approach can offer the best of both. For this approach, consider 70–80% of your portfolio for low-cost, passive ETFs—the “core”—anchoring your wealth to long-term market performance. Use the remaining 20–30% as your “satellite” allocation for active strategies, specific themes, or unique short-term market inefficiencies.

This gives you what might be called a “mistake budget”: room to explore, without jeopardizing the stability of your overall plan.

Ultimately, it may be time to reframe the question altogether. Instead of asking, “Should I invest actively or passively?” a better question might be:

“Am I gaining exposure I can’t get through a benchmark? Is there a genuine inefficiency here that active management can exploit?”

If not, the passive route—steady, disciplined, and low-cost—will likely serve you best over the long run.

What About Short- and Intermediate Term Investors?

The difference still holds true for short- and intermediate-term investors, with one caveat.

The difference in one’s ability to reach their goals is not as profound as for long-term investors, because compounding doesn’t have the same power over shorter periods.

That said, there are some reasons why an investor might be willing to give up some return for the potential to maintain stronger downside hedging.

Active management may suit shorter-term goals when:

You need downside protection (less volatility)

You’re targeting a specific return window (e.g., 5–10 years)

You have a strong view on market inefficiencies

But over long periods of time, even a difference of 1% average annual return can mean the difference of hundreds of thousands of dollars.

So the argument can sometimes sway more toward active funds for specific situations, goals and risk tolerances. That’s why it’s important to speak with a financial professional prior to making significant financial decisions, especially if you are feeling uncertain.

What’s the Answer?

For most long-term growth goals, one logical answer is to use passive ETFs as the core strategy.

Why? Because they offer:

Lower fees → more compounding

Tax efficiency → less drag

Flexibility and transparency

Diversified exposure with fewer hidden costs

When might mutual funds make sense?

If you’re targeting an intermediate-term goal (e.g., 5-10 years) and believe in a specific active manager’s capability.

If you’re investing via a platform that only offers certain mutual funds.

If you’re seeking very specific niche strategies where active mutual funds still dominate.

- If you’re investing in fixed income (such as bonds), in small-cap stocks, or in international stocks. These types of investments often see a more encouraging degree of success from active management.

Blended approach = best of both worlds:

Core portfolio: broad-market ETFs (domestic + international equities, bonds)

Satellite sleeve: a handful of mutual funds (active strategies) or thematic ETFs to capture potential alpha

Regular rebalancing and monitoring of correlation and risk (diversification not just by number of holdings, but by behavior, meaning low correlation across sleeves)

In other words: while ETFs are generally the better choice for the “engine” of your portfolio, mutual funds can play a strategic role.

The key is alignment with time horizon, cost sensitivity, portfolio allocation, and tax context.

Conclusion

In the long-term growth race, every basis point counts.

The difference between an ETF and a mutual fund is less about which is better in an absolute sense and more about which aligns better with your goals, time horizon, cost sensitivity, tax situation, and portfolio construction.

For the vast majority of investors targeting a 10-, 20- or 30-year horizon, low-cost passive ETFs offer a compelling path: holding broad diversification, minimizing fees, and reducing tax drag—all while letting time do the heavy lifting.

Mutual funds still have a role—particularly for intermediate goals or when you’re willing to pay for active management to reduce overall portfolio risk. The optimal portfolio often blends both.

As you build your wealth, focus on the fundamentals: costs, tax efficiency, diversification, asset-allocation discipline, and staying the course. Choose the vehicle that best supports those fundamentals, whether that ends up being predominantly ETFs with a smaller mutual fund sleeve or a different mix entirely.

If you’d like to dig deeper into how to select specific ETFs and mutual funds, how to evaluate active managers, or how to monitor and rebalance your blend over time, I welcome you to join the exclusive community at The Wealth Expedition. Let’s build not just your portfolio—but your mindset, discipline and long-term freedom together.

For Further Reading, Check Out:

The Art & Science of Investing: How to Invest and Get Rich the Right Way

The Roth IRA: Pay No Tax On This Retirement Income

Know This Before Choosing Dividends, Interest or Capital Gains

The Index Fund: Is Passive Management Worth the Low Cost?

Do Risk-Free Investments Exist?

Asset Allocation: Are You Getting Your Best Return?

How to Increase Retirement Income (Without Running Out of Money)

How Much Do I Need to Save for Retirement?

Psychology of Investing: Why Fear Costs More Than Failure Ever Could